| |

When we began the Community Solar Value Project, we held a clear vision of shared-solar projects that would bring the utility and its customers together in a market-based demonstration of several DER strategies needed for an integrated and flexible grid. We envisioned tapping strategic solar siting and design plus DR and storage “companion measures”—orchestrated to help balance the load and increase the net value of local PV. Now, a year later, we’re almost there, except for a few challenges, including one in the guise of low-cost centralized solar.

Yes, it is hard to turn down a cheaper solar option. According to the Solar Energy Industries Association and GTM Research, solar costs fell last year to less than $1.50 per Watt for utility-scale fixed-tilt systems. If you were doing community solar primarily to deliver savings to subscribers, this might look like an answer. A number of utilities are now planning voluntary programs that tap big solar and package it kind of like wind-based green-power programs. Even community solar on the distribution grid is going to the urban fringe. In Minnesota, community solar developers have been co-locating 1-MW projects to reach economies of scale, with the state limiting developers to five co-located projects.

At the Community Solar Value Project (CSVP), we always recognized the benefit of scale. But we are focused on distribution-system projects, and preferably infill projects in the 500-kW to 2-MW range. Why? Well, one of our core assumptions is that distributed solar is here to stay. Whether or not the utility is involved, customers will pursue distributed solar. But if the utility were involved, the pairing of these large-commercial scale projects with DR and storage options (and in some cases, energy efficiency) represents what we call a “market-based laboratory” for field-testing many of the smart-grid and flexible-DER strategies that are currently stuck at the white-paper stage or in isolated pilot programs. As far as we know (and tell us if we’re wrong) no one has yet market-tested the economics of a distributed solar fleet strategy (achieving, say, 10 MW through a fleet of community-solar projects). Certainly there is little testing of distributed solar strategies that incorporate high-value companion measures. Sources like GTM Research and Rocky Mountain Institute and ICF International all have recently touted the distributed-energy future. And, for the most part, we believe them. But implementation in existing utility cultures, including engagement with and learning from “real” customers, is a project that needs to start now. The smart grid will not emerge fully armed, like Athena, from the head of Zeus. It will emerge from a trail of better and bigger attempts to get the thing right.

The CSVP recently started to work on an effort called “Filling the Pricing Gap,” to help utilities create and justify more competitive community-solar pricing for programs based (at least primarily) on local PV resources. You will see presentations and reports on our progress here in coming weeks. The folks at the Sacramento Municipal Utility District have been walking this road with us—or more accurately, they are usually in the lead, as they apply tremendous experience and in-house expertise to the challenge. One early example: they have taught us that a conventional “value of solar” argument is not such a practical solution for justifying near-term program design. For one thing it makes most utility guys’ hair stand on end. For another, it raises endless “what-if” questions about increasingly dynamic technical options, markets, and policies.

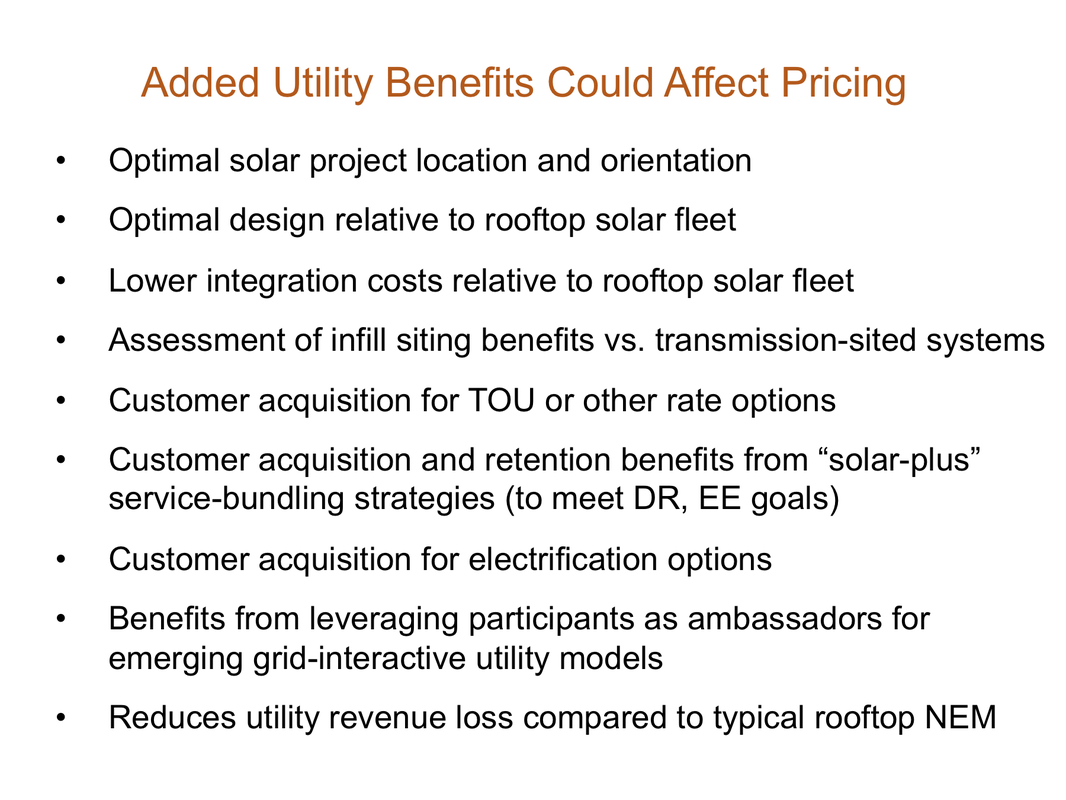

While others look for a VOS algorithm that would be, in effect a “theory of everything” for DER, we work to combine a relative few, fairly indisputable aspects of VOS analysis with targeted strategic arguments. This includes presenting what we call “realistic hypotheticals,” scenarios with ranges of numbers that are not intended to hit the value nail on the head, but which are nevertheless worth considering.

I use plural because we are addressing multiple internal stakeholders in the utility, all of whom have strong (and often conflicting) points of view. We are also addressing the utility’s most timely concern—that it needs to build and maintain strong customer relationships throughout these trying times. Watch our Library and Workshops pages for our reports from the field—where at least for the most part, we are keeping it local.

Yes, it is hard to turn down a cheaper solar option. According to the Solar Energy Industries Association and GTM Research, solar costs fell last year to less than $1.50 per Watt for utility-scale fixed-tilt systems. If you were doing community solar primarily to deliver savings to subscribers, this might look like an answer. A number of utilities are now planning voluntary programs that tap big solar and package it kind of like wind-based green-power programs. Even community solar on the distribution grid is going to the urban fringe. In Minnesota, community solar developers have been co-locating 1-MW projects to reach economies of scale, with the state limiting developers to five co-located projects.

At the Community Solar Value Project (CSVP), we always recognized the benefit of scale. But we are focused on distribution-system projects, and preferably infill projects in the 500-kW to 2-MW range. Why? Well, one of our core assumptions is that distributed solar is here to stay. Whether or not the utility is involved, customers will pursue distributed solar. But if the utility were involved, the pairing of these large-commercial scale projects with DR and storage options (and in some cases, energy efficiency) represents what we call a “market-based laboratory” for field-testing many of the smart-grid and flexible-DER strategies that are currently stuck at the white-paper stage or in isolated pilot programs. As far as we know (and tell us if we’re wrong) no one has yet market-tested the economics of a distributed solar fleet strategy (achieving, say, 10 MW through a fleet of community-solar projects). Certainly there is little testing of distributed solar strategies that incorporate high-value companion measures. Sources like GTM Research and Rocky Mountain Institute and ICF International all have recently touted the distributed-energy future. And, for the most part, we believe them. But implementation in existing utility cultures, including engagement with and learning from “real” customers, is a project that needs to start now. The smart grid will not emerge fully armed, like Athena, from the head of Zeus. It will emerge from a trail of better and bigger attempts to get the thing right.

The CSVP recently started to work on an effort called “Filling the Pricing Gap,” to help utilities create and justify more competitive community-solar pricing for programs based (at least primarily) on local PV resources. You will see presentations and reports on our progress here in coming weeks. The folks at the Sacramento Municipal Utility District have been walking this road with us—or more accurately, they are usually in the lead, as they apply tremendous experience and in-house expertise to the challenge. One early example: they have taught us that a conventional “value of solar” argument is not such a practical solution for justifying near-term program design. For one thing it makes most utility guys’ hair stand on end. For another, it raises endless “what-if” questions about increasingly dynamic technical options, markets, and policies.

While others look for a VOS algorithm that would be, in effect a “theory of everything” for DER, we work to combine a relative few, fairly indisputable aspects of VOS analysis with targeted strategic arguments. This includes presenting what we call “realistic hypotheticals,” scenarios with ranges of numbers that are not intended to hit the value nail on the head, but which are nevertheless worth considering.

I use plural because we are addressing multiple internal stakeholders in the utility, all of whom have strong (and often conflicting) points of view. We are also addressing the utility’s most timely concern—that it needs to build and maintain strong customer relationships throughout these trying times. Watch our Library and Workshops pages for our reports from the field—where at least for the most part, we are keeping it local.

A sampling of benefits that utilities might consider to "close the pricing gap" for distributed community solar.